|

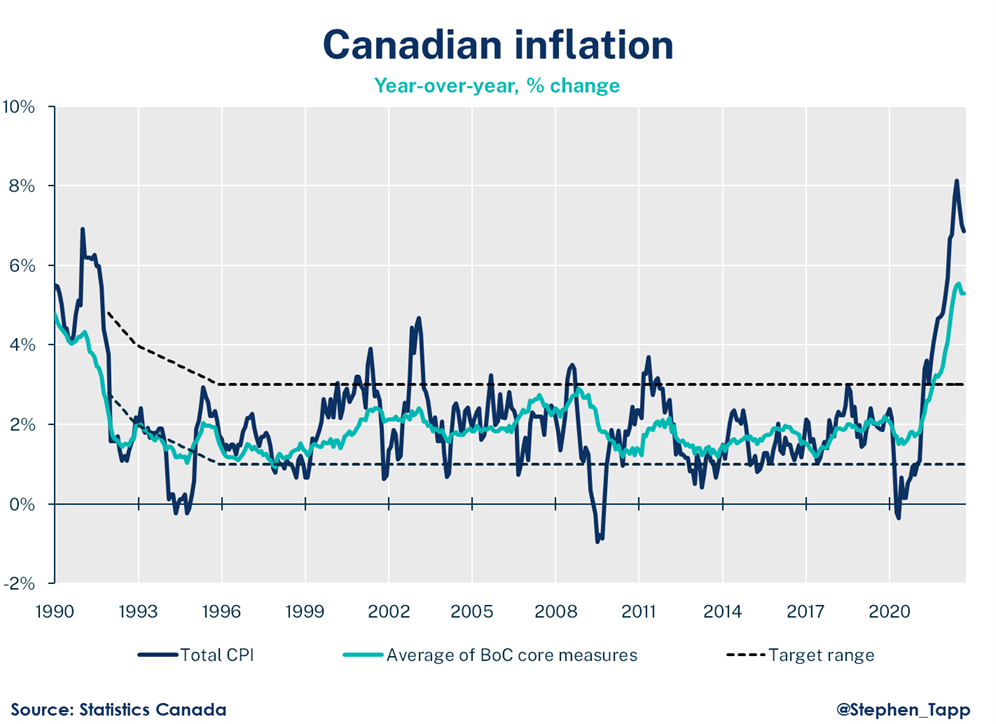

As expected, the Bank of Canada held off on changing its target interest rate. The move signals that efforts to curb inflation are working. The forecast is for inflation to keep falling and reach 3% by summer. Statistics Canada will provided its next update on the Consumer Price Index on March 21.

It's Budget Season for all levels of government. After the province reveals BC Budget 2023 on Feb. 28, the federal government will announce its own budget at some point in the following weeks. Municipalities in BC don't have the same flexibility, with legislation requiring financial plans be adopted by March 31 and tax rate bylaws before May 15.

The Chamber is working to remind Greater Victoria municipalities that they need to support their community's businesses through fair taxation. We encourage Chamber members to get involved with their local government through however they can. In the City of Victoria, for example, Council is asking The Chamber for member feedback on a 6.96% increase to residential property taxes that's largely the result of inflation. While that's down from the almost 9% increase initially proposed in January, there might be more opportunities to find efficiencies. Businesses that pay property taxes in Victoria are urged to voice their formal feedback by:

If you have questions or concerns about municipalities outside Victoria, please let us know by emailing communications@victoriachamber.ca. And watch for more coverage on The Chamber's budget advocacy on social media and in upcoming editions of BizNews. Could this be the end of interest rate increases? The Bank of Canada increased its rate today to 4¼%, but softened the language it uses around future increases.

A statement from the bank said the bottlenecks that had been affecting global supply chains are loosening. The Consumer Price Index was at 6.9% in October, though core inflation was 5% — much closer to the bank's target of 2%. "Three-month rates of change in core inflation have come down, an early indicator that price pressures may be losing momentum," the bank stated. "However, inflation is still too high. The longer consumers and businesses expect inflation to be above the target, the greater the risk that elevated inflation becomes entrenched." Make sure to consult with your preferred financial and mortgage advisors —The Chamber's Member Directory is a great place to find experts who can help you make your business thrive. Businesses that service the real estate industry are a major contributor to Greater Victoria's economy. However, rising interest rates have slowed sales. Throw in the traditional quiet period around the holidays and fewer properties are changing hands. Only 384 sales were recorded in the region for November, down from 653 last November.

There are also concerns about potential unintended consequences of recent changes to the provincial Strata Property Act. "It is an open question whether these changes will bring any additional rental stock to the market — with BC's complex Residential Tenancy Act not all homeowners of vacant strata homes have a desire to become landlords and current interest rates are less attractive to investors who may want to purchase strata rental properties," Victoria Real Estate Board President President Dinnie-Smyth said in a news release. "It is also possible that these measures will contribute further to eroding housing affordability as older stratas with rental restrictions were generally valued lower than their rentable counterparts." Slower sales have also contributed to a slight dip in market values over the last few months. That could mean some property assessments — being sent out soon to homeowners from BC Assessment — will be higher than current market value. “I want to emphasize that assessments are based on July 1 values of this year, meaning that when similar properties were sold up to and around July 1, those market value sales are used to calculate your assessed value," Assessor Bryan Mura said in a news release. “An increase in assessment value does not, however, necessarily result in an increase in property taxes. Taxes are typically only affected if you are above the average value change for your community." Inflation has become the top concern for many businesses. The Chamber is hearing from many members struggling to balance higher costs by adjusting prices and raising wages to keep staff.

On top of this, the increased emphasis on tipping that took hold during the pandemic has created new challenges for employers, employees and customers. The issues and a few solutions are the subject of a new series that recently ran in the Times Colonist. The articles shine a light on how tipping was affected by social changes over the past few years, as well as consumers reliance on debit cards and tax implications for people whose income relies on tips. It's well worth the read as we head into the holiday shopping season!  Changing times create disruption but also present tremendous opportunities for forward-thinking organizations. The tide of high inflation has highlighted the need to create more resilient local production and supply networks.

Groceries are a good example of the need for investment in suppliers located closer to home. The provincial government's Buy BC program and the Vancouver Island Economic Alliance's Island Good shows the value of supporting innovation led by business. On Monday, BuyBC hosted an event in Victoria called Every Chef Needs a Farmer, Every Farmer Needs a Chef. Among the exhibitors was Finest at Sea Ocean Products. "There is clear evidence of the value that bring local brings to a community, but it's not always top of mind when we're at the grocery story purchasing produce for our families," Chamber CEO Bruce Williams said. "The Buy BC and Island Good programs makes it easier to remember the value in buying local, both in terms of freshness and health as well as in ensuring local farmers feel they are supported so they can take the risks needed to build their business." To paraphrase that old Isley Brothers hit, it's not quite time to "Shout," but inflation is trending "a little bit softer now." The latest figures from Statistics Canada show the pace of inflation slowed in September, with the cost of goods rising 6.9% from a year earlier. Inflation has been declining for three months, after peaking at 8.1% in June. The sharp rise in costs was initially attributed to fuel shortages caused by the war in Ukraine, a super-heated housing market and supply chain disruptions caused by the pandemic. However, fuel costs have stopped rising as sharply and supply chains are getting close to their typical efficiencies. "However, these gains were largely offset by the continued rise of prices for food and services. Unfortunately, there was no progress on 'core' inflation, which held steady at 5%," Canadian Chamber of Commerce Chief Economist Stephen Tapp said. "Today’s lack of progress on inflation — together with Bank of Canada surveys released earlier this week that suggested inflation expectations remain elevated — should be concerning enough to the Bank of Canada for them to deliver the 50 basis-point interest rate hike that the market expects (Oct. 26)."  |

Copyright © 2021 Greater Victoria Chamber of Commerce. All rights reserved.

#100 – 852 Fort St., Victoria, BC V8W 1H8, Canada | Phone: (250) 383-7191

chamber@victoriachamber.ca | Site Map

#100 – 852 Fort St., Victoria, BC V8W 1H8, Canada | Phone: (250) 383-7191

chamber@victoriachamber.ca | Site Map

Notice a typo or broken link? Please let us know so we can fix it ASAP. Email communications@victoriachamber.ca